Valuation (DCF, Comparable) Your Ultimate Guide to Understanding Business Worth

The ability to valuation a business is an essential skill for investors, analysts, and entrepreneurs. Being informed about what a business or asset is really worth allows for Smarter financial decisions — whether it is buying stocks, selling a company, or raising capital. The two most common ways to value a business are Valuation (DCF, Comparable) (also referred to as multiples). All have a different spin & give something to think about.

How Valuation (DCF ) Works

In this post, we’re going to dissect how DCF works, detail the formula step by step, guide you through a simple example, and discuss the pros and cons of both methods. You will also come across answers to some common questions and a very simple conclusion that Summarise everything.

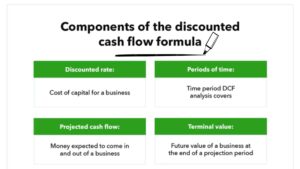

Here is the thought process: A dollar today is worth more than a dollar tomorrow because you can invest that dollar and earn a return. In order to do this, DCF reduces the value of future cash flows to include only the values today, discounted by a discount rate. And this discount rate would often reflect the riskiness of those cash flows — usually the company’s Weighted Average Cost of Capital (WACC).

Step-by-step process of Valuation (DCF)

Predict future cash flows: Calculate how much cash the company will produce each year for a fixed period, and that period’s typically 5-10 years.

Compute the terminal value: Because firms last forever (conceptually), determine the value of all cash flows that occur after the end of the forecast horizon.

Discount cashflows: Use the discount rate to find the present value of future cash flows (including the terminal value).

Sum all discounted cash flows: This total is the estimated intrinsic value of the business.

DCF is highly regarded for its detailed, fundamentals-driven approach, but it requires solid assumptions about growth rates, margins, and capital costs.

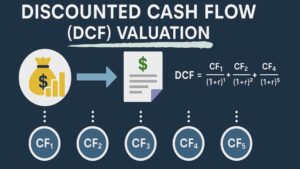

The DCF Formula Explained.

At the core of the DCF method is a straightforward formula:

Where:

-

= Cash flow in year t

-

r = Discount rate (typically WACC)

-

t = Year (1 through n)

-

n = Number of forecasted years

-

TV = Terminal value at the end of year n

Terminal Value Calculation

There are two common ways to calculate terminal value:

Perpetuity Growth Model: Assumes cash flows grow at a steady rate forever.

![]()

Where g

g is the constant long term growth rate (usually a pessimistic number, such as inflation or GDP growth)

Exit Multiple Approach: Applies a comparable company’s valuation multiple (i.e. EV/EBITDA) to calculate terminal value.

Which method is best depends on the company and the particular industry.

Valuation (DCF) Example .

Let’s make this a little more concrete with a simple example.

Suppose you are trying to value a company that will generate $100,000 in free cash flow next year. You estimate that cash flows will increase at an average rate of 5% per year for the next 5 years. The WACC is 10%, and you estimate a terminal growth rate of 3%.

Step 1: Forecast Cash Flows

Year Cash Flow (CF)

1 $100,000

2 $105,000 (100,000 * 1.05)

3 $110,250

4 $115,763

5 $121,551

Step 2: Calculate Terminal Value .

![]()

Step 3: Discount Cash Flows & Terminal Value to Present Value

Using the formula for each year:

Year CF / (1 + r)^t

1 $100,000 / (1.10)^1 = $90,909

2 $105,000 / (1.10)^2 = $86,777

3 $110,250 / (1.10)^3 = $82,858

4 $115,763 / (1.10)^4 = $79,152

5 $121,551 / (1.10)^5 = $75,679

Terminal Value $1,788,529 / (1.10)^5 = $1,113,324

Step 4: Sum Present Values

Total DCF value = Sum of discounted cash flows + discounted terminal value

= $90,909 + $86,777 + $82,858 + $79,152 + $75,679 + $1,113,324

= $1,528,699

That means this businesses value according to your estimation is around $1.53 million.

Comparable (Multiples) Valuation : A Quick Snapshot

Comparable valuation Common multiples used include:

Price to Earnings (P/E) ratio

Enterprise Value to EBITDA (EV/EBITDA)

Price to Sales (P/S) ratio

How Comparable Work

- Identify similar companies (same industry, size, growth prospects).

- Calculate their valuation multiples.

- Multiply the company’s metric by the average or median multiple.

One scenario could be this: If industry peers trade for on average 8x EV/EBITDA and your company generates $200,000 of EBITDA your company value could potentially be:

( Value=8×200,000=1,600,000 )

Comparable are fast and market-based, so they are popular for benchmarking.

Pros and Cons of DCF and Comparable

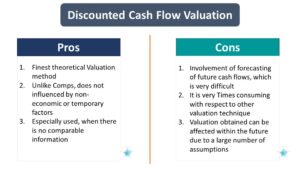

DCF Pros :

- Value emphasis: Fundamental based on value.

- Flexible: Detail model for growth and capital structure.

- Forward looking: Is based on a long time business perspective.

DCF Cons:

Assumption-intensive: Small alterations in assumptions (growth rate, discount rate) can radically alter outcomes, and options mechanics inevitably introduce a lot of gray area.

Data driven: Relies on high-quality financial forecasts and knowledge of capital expenses.

Complex: Beginners will find it not always intuitive.

Comparable Pros:

- Easy and fast: Simple to compute with commonly available information.

- Market-based: Based on the prevailing investor mood and industry trends.

- Helpful for benchmarking: It can be used to position a company among industry peers.

Comparable Cons:

- Market noise: Bubbles or crashes in the market can distort multiples.

- Disregards basics: Does not look at individual business strengths and weaknesses.

- Finding perfect peers: Actually, it’s hard to find truly comparable companies.

FAQs About Valuation (DCF and Comparable)

Q: Which valuation method is better?

A: There is no one method that is better than the other — they do different things. DCF is good for deep analysis when you have solid data, and comparable give you a fast and easy market-based estimate. Ditto for using them both together: That’s often the best way to gain insight.

Q: How do I choose a discount rate for DCF?

A: The discount rate tends to be equal to the firm’s weighted average cost of capital (WACC), which is the cost of equity and debt accounting for risk.

Q: Can the DCF model work for a startup?

A: It’s hard because startups generally don’t have stable sources of cash flow. When it comes to those, comparables or other valuation methodologies (e.g., VC-based methods) are the best.

Q: What’s a terminal growth rate?

A: It is the rate at which the cash flows are expected to grow indefinitely after the forecasted period. It should be a conservative one — typically one that grows with inflation or G.D.P.

Q: Can market multiple be misleading for investors?

A: Yes, especially in periods of market euphoria or fear. It is also important to look at fundamental business principles as well.

The Bottom Line

Valuation, Valuation is core to finance, and if you understand both DCF (“Discounted Cash Flow“) and Comparable, you get two somewhat overlapping but complementary, perspectives into what a company is worth. DCF takes a deeper look into the business details of Baidu, and based on logic and facts in the market, the stock’s intrinsic value is calculated. For comparable, in contrast, it’s a reality check on the market of how similar businesses are priced.

By utilizing these approaches, investors can double-check estimates and make better decisions. Whether you are an investor, raising capital, or selling a business, if you know how to use these tools, you will be better equipped to look past the price tags on the surface and pin down just what something is truly worth.

Thank you