Corporate Finance – (FINANCIAL STATEMENT)

Corporate Finance is a field of finance that deals with how corporations handle their financial activities and decisions. It focuses on

- Capital Budgeting – How a company decides which long-term investments to take on

- Capital Structure – How a company finances its operations (e.g., through debt, equity, or a mix).

- Working Capital Management – Managing short-term assets and liabilities to ensure a company can meet its day-to-day obligations.

- Dividend Decisions – How much profit a company returns to shareholders versus reinvesting.

- In short, corporate finance is about maximizing shareholder value through sound financial planning and strat

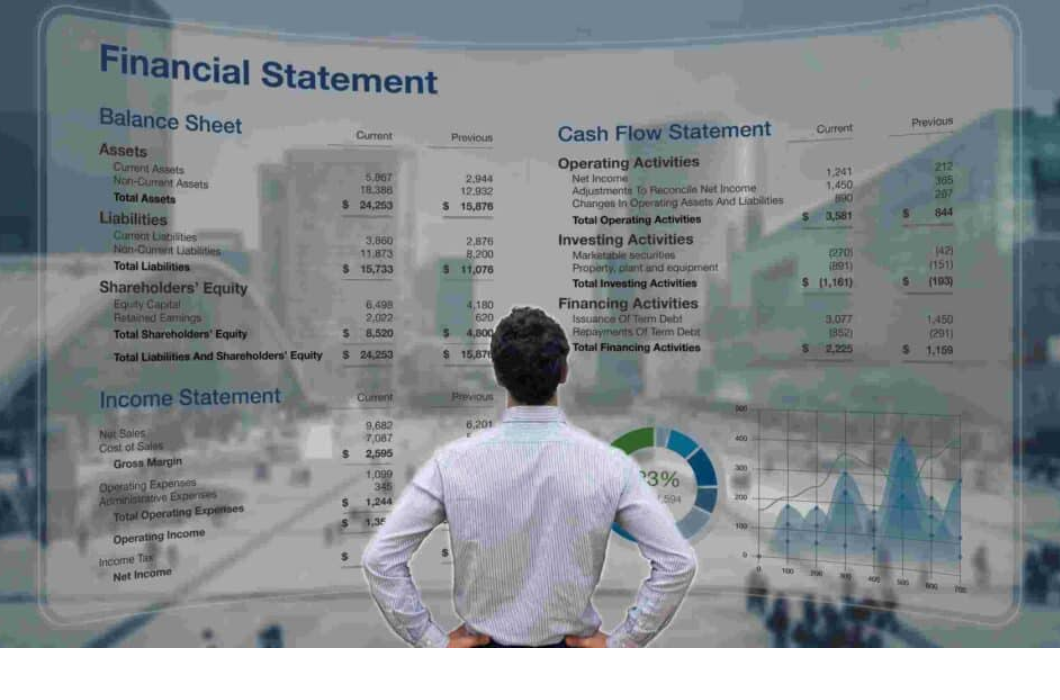

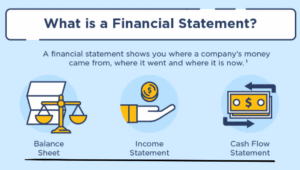

Q . What Is a Financial Statement? (Balance Sheet & Income Statement Explained)?

- Financial statements are official records of a firm’s financial performance and health over a particular period. They become even more indispensable instruments for investors, employers, and the community to make decisions. The most important of these are the balance sheet and the income statement.

The statement of financial position (balance Sheet)

- A balance sheet in part reveals what a company owns (its assets), what it owes (its liabilities) and the value of the company to its stockholders (the shareholders’ equity) as of a specific date. It is formulated as

- Equation of the Balance Sheet (Assets = Liabilities + Shareholders’ Equity)

- Assets – What the company has (i.e. cash, inventory, equipment).

- Liabilities – What the company owes (i.e., loans, accounts payable).

- Equity – A portion of a company’s assets that belongs to its owners once liabilities are deducted.

- The best analogy might be a financial snapshot of the company’s health.

Profit and Loss (P & L)

- The first financial statement is the income statement, which shows a company’s revenue, expenses and ultimately its profit or loss over a period of time (month, quarter, year).

- Expense – Net Income is calculated as follows: Revenue

- Revenue – Money you make selling products or services.

- Costs – These are the expenses you will have to bear such as salaries, rent, materials.

- Net Profit or Net Loss – Profit (or loss) after all expenses.

Q . Why Do These Statements Matter ?

- Investors rely on them to gauge profitability and financial fitness.

- They’re also used by management to help inform decisions and strategy.

- They are used by lenders to assess creditworthiness.

- They are tools for regulators in fostering compliance and transparency.

Q . How Financial Statements Work ?

1. The Income Statement (Earnings and spending of the company)

- The income statement is a record of a company’s performance over time (typically during a month, a quarter, or a year). It begins with revenue and then takes away any and all associated costs and expenses to count the net income (profit or loss).

Example Workflow

- Revenue (Sales): $100,000

- Cost of Goods Sold (COGS): $40,000

- Gross Profit = Sales-Expenses Gross Profit = $100,000 – $40,000 = $60,000

- Operating Expenses: $30,000

Net Income (Profit) = $30,000−$5,000 = $25,000

This lets you know whether the business was profitable or lost money.

2. Balance Sheet (What the business has and what it owes)

- The balance sheet is a snapshot in time of the company’s financial position. It always balances:

- Assets = Liabilities + Equity

Example Balance Sheet:

- Assets

Cash: $20,000

Equipment: $50,000

Inventory: $10,000

Total Assets = $80,000 - Liabilities

Loans: $30,000

Accounts Payable: $10,000

Total Liabilities = $40,000 - Equity

Retained Earnings + Owner’s Equity: $40,000

Total Equity = $40,000

Q. How They Work Together

Net income on the income statement feeds into the equity section of the balance sheet (on “retained earnings”).Profits are equity building; losses are equity draining. This linking mechanism ensures that all financial statements tell a single, integrated story.

-

Statement

Income Statement , How much was received and expended , Over some time period

Balance Sheet, What is owned and owed (net worth) , Point in time

Untitled design Untitled design

Key Points:

1 Financial Statements Definition

-What are financial statements and why they are important in business.

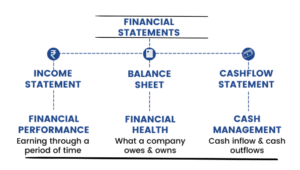

2 . Key Financial Statements

Concentrate on the balance sheet and the income statement (mention others, such as the cash flow statement, in passing or don’t mention them at all).

3 . Purpose of Each Statement

Balance Sheet: How much you own and how much you owe.

Income Statement: Follows the flow of revenue, expenses, and profit across time.

4. Structure & Components

Balance sheet: assets, liabilities and equity.

Income statement: revenue, cost of goods sold, gross profit, expenses, net income.

5 -How They Work Together

The income on the income statement increases retained earnings on the balance sheet.

6.Importance for Stakeholders

Employed by investors, managers, lenders and regulators to make decisions.

7.Examples or Templates

Sample and real-world layout examples for users to see and their understanding.

8.Mistakes or Misconceptions

Misconstruing profit and cash flow, or liabilities vs. expenses.

9.Advantages of Financial Statements

Improved: Financial planning, performance and transparency.

10. Who Uses Financial Statements.

Start-ups, companies, accountants and investors.

Comparison: Old vs New Financial Statements

- Aspect , Old Financial Statements , New Financial Statements

Preparation Method , Manual (paper-based, spreadsheets) , Digital tools (accounting software, cloud-based systems).

Speed & Frequency , Quarterly or annually, with delays , Real-time or monthly updates possible

Accuracy & Errors , High chance of human error , Automated checks, improved accuracy

Access & Sharing , Physical copies, hard to distribute , Instantly shareable online, accessible remotely

Analysis Tools , Basic ratios done by hand , Advanced analytics, dashboards, AI-powered insights

Data Integration , Standalone statements Linked with invent ory, payroll, CRM, etc.

Compliance Standards , Local or inconsistent standards , Unified frameworks (e.g., IFRS, GAAP), globally adopted.

Presentation Style , Static tables, minimal visiual , Interactive dashboards, charts, trend analysis

Stakeholder Use , Mainly internal, or auditors . ,Used by investors, m regulators, lenders, and AI-based decision systems.

Security & Backup , Prone to loss/damage , Cloud storage with encryption and regular backups

Key Shift Drivers

- Tech: Cloud accounting (such as QuickBooks, Xero) takes care of reporting.

- Globalisation: Requirement to have uniform standards across borders (IFRS/GAAP).

- Data-Driven Decision Making: Increased appetite for instant and actional insights.

- Compliance & Transparency: Tighter regulatory, investor demands.

He development of financial statements

First Ancient Beginnings (Pre-15th Century)

- Ancient Accounting: Primitive forms of accounting appeared in ancient civilizations such as Mesopotamia and Egypt as early as 3300-2000 BC to organize their trade, taxation, and resource allocation.

Double-entry bookkeeping was not yet invented, but merchants in ancient Greece, Rome and the Byzantine Empire started entering debits and credits in crude ledgers.

The Advent of Double-Entry Bookkeeping (15th Century)

- 1494: The breakthrough was the work of an Italian mathematician and Franciscan friar, Luca Pacioli. His Summa of Arithmetic inspired the double-entry bookkeeping system. This system provided the foundation for the balance sheet, under which each transaction has two effects: a debit and a credit.

Balance Sheet: Pacioli’s method led to the development of tracking assets, liabilities, and equity in a systematic and accurate manner.

The Industrial Revolution (18–19th century)

- Growing Complexity: Businesses that grew in size during the Industrial Revolution required more sophisticated financial reporting to monitor their performance, control their costs, and attract investment.

Balance Sheet and Income Statement: The demand for more formal and uniform accounting procedures during this period hastened the acceptance of the the balance Sheet and income statement. These two documents formed the basis of financial reporting, but were much less uniform at the time than they are today.

1900s Early 20th Century (1900-1939)

- Standardization and Regulation: With companies growing more sophisticated and financial markets expanding, calls were made for the standardization of accounting to enhance transparency and comparability.

1913: The American Institute of Certified Public Accountants (AICPA) was established to provide guidance on accounting practices.

1929-1930s: The Great Depression exposed the importance for improved corporate transparency and more robust financial reporting.

1933 & 1934 The Securities Act of 1933 and the Securities Exchange Act of 1934 laid the foundation for how companies would report financials, forcing them to report more detailed and precise financial data—such as balance sheets and income statements.

Mid-20th Century (1940s-1980s)

- Globalisation Global trade was increasing and the international accounting standards were created to align accounting practices beyond borders. This course has enabled multi-national companies to implement uniform accounting statements.

The standard to follow in the U.S. under Generally Accepted Accounting Principles was established and guidance to structuring financial statements was made available.

Late 20th Century-Present (1990s-Present)

- Computerization: With the arrival of computer technology and accounting software in the later part of the 20th century, many accounting tasks, such as posting transactions and issuing reports, can now be done in minutes and reports can be generated instantly.

International Standards: The IFRS was adopted by countries across the world (except for the U.S., which still uses GAAP). This move enabled financial statements to be more easily comparable across different markets and regions.

Real-Time Reporting The proliferation of cloud-based accounting software (QuickBooks Online, Xero, etc.) now enables companies to keep their balance sheet and income statement up-to-date on a daily basis, which helps give stakeholders relevant information faster.

Financial Statements: The Future

- Automation and AI: Financial statements are increasingly becoming automated and more accurate, thanks to AI and machine learning. AI tools have moved from mining financial data for insights to predicting trends and even creating financial reports.

Blockchain: The impact of blockchain technology is not one that we can overlook, and we’re seeing a great deal of promise in securing and maintaining integrity around financial reporting, particularly with respect to transaction verification.

You Mean by Michael LaBianca with Pashion lessons-a/Contributions Lopedia Defining

- 1494: Luca Pacioli and his double-entry bookkeeping.

- 1929-1934: A regulatory framework was put in place in the U.S. following the Great Depression.

- 1973: The International Accounting Standards Committee (IASC) is established.

- 2001: Widespread adoption of IFRS in many countries.

- 21st Century: The emergence of cloud financial tools and artificial intelligence reporting.

Conclusion

- From the rudimentary records of ancient transactions, to modern complex financial statements, the balance sheet and income statement serve as a foundation for understanding a company’s financial standing, and they will each be further explored in this series’s forthcoming monthly columns. Today, it is an essential element of corporate governance, investment analysis, and financial decision making across the globe.

Pro Tip

- Grasp Financial Statements Relationships

When using the financial statements (balance sheet and income statement) remember these are in concert with one another. Those two reports are not independent from one another; they comprise a whole financial representation of a company.

Key Matchup: Il

- The income statement shows a company’s profit over a period of time (think like free cash flow!), and the net profits flows directly into a specific part of the equity part of the balance sheet (under “retained earnings”).

If a company is profitable, its equity increases, which means it has a stronger financial standing.

When a business has a loss (negative net income), the value of the business’s equity falls, decreasing the value of the business and threatening the business’s financial position.

How to Use This Knowledge

- Analyze: Don’t look at each financial statement in a vacuum when you consider your financial statements. How changes in Income Statement affect Balance Sheet.

Ask Questions: If the income statement looks great, but the balance sheet is reflecting inordinate debt or low equity, dig further to understand the true financial health of the company.

Watch for Red Flags: A decreased income (losses) can cause retained earnings to decrease which could lead to financing and/or investor trouble. Long term losses may sap equity.

[…] Easy Step to Guide Financial Statements , read more […]